| front |1 |2 |3 |4 |5 |6 |7 |8 |9 |10 |11 |12 |13 |14 |15 |16 |17 |18 |19 |20 |21 |22 |23 |24 |25 |26 |27 |28 |29 |30 |31 |32 |33 |34 |35 |36 |37 |38 |39 |40 |41 |42 |43 |44 |45 |46 |47 |48 |49 |50 |51 |52 |53 |54 |55 |56 |57 |58 |59 |60 |61 |review |

|

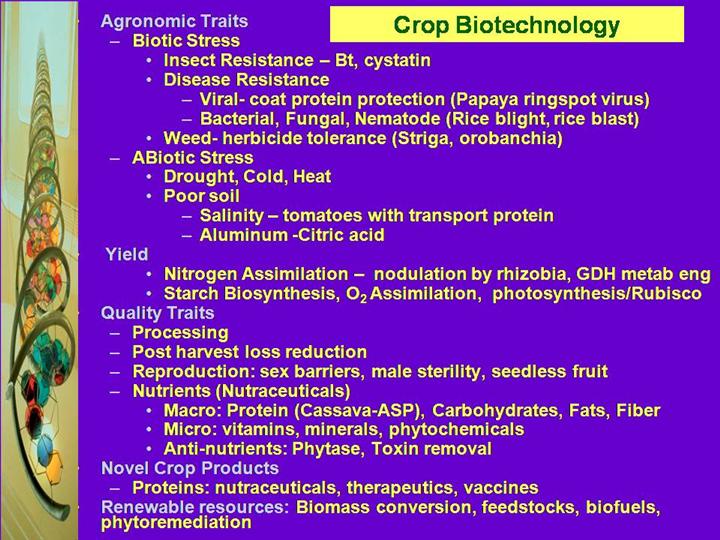

PROGRESS TO DATE Genetic modifications of crop plants can be organized into two broad-based non-mutually exclusive categories: those that benefit the producer and those that benefit the consumer. Modifications that protect the crop from either biotic stress (e.g., damage by predators such as insects and nematodes; diseases caused by viruses, fungi, bacteria; and weeds) or abiotic stress (e.g., drought, cold, heat, and poor soils) or increase total crop yield benefit the producer and are called “input traits.” The majority of modified crops in commercial use fit in this group. Scientists have just begun to tap the large potential of biotechnology to produce varieties of plants that confer a wide spectrum of advantages to consumers. These varieties are modified with “output traits.” The estimated global area of transgenic or genetically modified (GM) crops for 2001 is 52.6M ha (130.0 million acres), grown by 5.5 million farmers in thirteen countries. In 2001, four principal countries grew 99% of the global GM crops.. The USA grew 35.7 million ha (68% of global total), followed by Argentina with 11.8 million ha (22%), Canada with 3.2 million ha (6%) and China with 1.5 million ha (3%); China had the highest year-on-year percentage growth with a tripling of its Bt cotton area from 0.5 million ha in 2000 to 1.5 million ha. in 2001 (other crops acreage is ). Globally, the principal GM crops were soybean ( 33.3 million ha, 63% of global area, maize (9.8 million ha 19%), cotton (6.8 million ha 13%), and canola (2.7 million ha 5%). The breakdown by country, crop and trait is illustrated in Figure 1 & 2 and Table 1 and 2. ( James, 2001) In the first 6 years since introduction, 1996 to 2001, a cumulative total of over 175 million ha (almost 440 million acres) of GM crops were planted globally and met the expectations of millions of large and small farmers. Rapid adoption and planting of transgenic crops by millions of farmers around the world, growing global political, institutional, and country support for biotech crops, and data from independent sources confirm and support the benefits associated with biotech crops (James, 2001). During this early phase of the plant revolution, the benefits of plant genetic engineering have been largely confined to farmers. From a consumer position however here has been a major reduction of up to 93% in the mycotoxin fumonosin on Bt maize as reduction in insect damage limits access to fungal spores. Currently, U.S. companies that are active in transgenic plant research spend far more money on research and development than they will receive as their share of profits from modified seeds, sales of which will amount to approximately $1.5 billion. Most companies, including those in Europe, envision a far more lucrative future when the plant revolution matures further. One possibility is the $500 billion market for foods in the United States. The next major phase of the plant revolution is emphasizing the engineering of value added traits in plants. These traits will be ones that are readily apparent to the consumer. Adoption of the next stage of biotech crops may proceed more slowly, as the market confronts issues of how to determine price, share the value, and adjust marketing and handling to accommodate specialized end-use characteristics. Furthermore, competition from existing alternative products will not evaporate. Pitfalls that have accompanied the first generation of biotech crops, such as the US trade dispute with Europe and Japan over approval and labeling of GM crops, will also affect the next stage of products. Some industry analysts believe the development of more end-use quality traits will largely dismantle the existing marketing system of “commodity” field crops. In other words, there will be a movement away from bulk handling and blending of undifferentiated crops under very broad grades and standards categories and toward a system that can meet more specialized needs of buyers, even to the point of preserving the identity of a crop from the farm to the user. The added costs of such specialized handling will have to be justified by the value of the new crops to buyers. The leading commodity in this value-added focus area is the field broadly defined as “functional foods.” The Institute of Medicine’s Food and Nutrition Board (IOM/NAS, 1994) defined functional foods as “any food or food ingredient that may provide a health benefit beyond the traditional nutrients it contains.” (Goldberg I, 1994 Hasler, 1998). The term nutraceutical was coined by the Foundation for Innovation in Medicine in 1991 (DeFelice, 1991) and is defined as "any substance that may be considered a food or part of a food and provides medical or health benefits, including the prevention and treatment of disease.” The nutraceutical industry has been viewed with renewed interest since the passage in October 1994 of the Dietary Supplement Health and Education Act (DSHEA). Before the passage of the DSHEA, regulations restricted the marketing of nutraceuticals, and companies’ limited their investment in research and development. Modifications in the regulations now make this market more appealing. One estimate states that foods that are used for nutraceutical purposes made up 10% of the value $503 billion total value of the U.S.Retail food market. (Food Labeling News. 1994) One of the major changes brought about by the DSHEA was the change in classification of dietary supplements from "food additives" which require FDA approval to "food" which does not. Another significant change was that dietary supplements might now be labeled with truthful claims about their medicinal benefits. Interestingly, while food supplement manufacturers can label their products with statements about health benefits, food manufacturers who sell foods fortified with the same nutrients may not. In addition, food supplements can now be marketed as conventional foods, which was prohibited under the former regulations. |